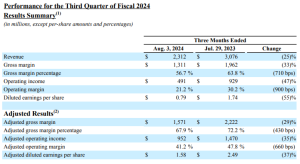

ADI’s revenue in the third fiscal quarter was $2.31 billion, down year-on-year but higher than expected.

The analog device giant ADI recently announced its financial report for the third quarter of the fiscal year 2024 ending on August 3. Its revenue was $2.312 billion, a year-on-year decrease of 25%; the gross margin was 56.7%, a year-on-year decrease of 7.1 percentage points; the operating profit was $491 million, a year-on-year decrease of 47%; the operating cash flow in the past 12 months was $4 billion, and the free cash flow was $2.9 billion.

Forecast: The overall average price increase of DRAM products in 2024 will be more than 50% to 60%.

According to the Sci-tech Innovation Board Daily citing Taiwan’s Electronic Times, benefiting from the dividends brought by AI business opportunities, the operations of major memory manufacturers continue to recover and grow. The market expects that driven by the surge in demand for HBM and the increase in the penetration rate of DDR5, the overall average price of DRAM products will continue to rise. In 2024, the average increase will reach about 50% to 60% or more. Although the base period has been raised, there is still a chance to maintain an increase of 30% to 40% in 2025. HBM will be the key that directly affects the supply and demand and price trends of the DRAM industry.

The average price of 8-layer stacked HBM is about 5 times higher than that of DDR5. And there is still much room for improvement in the yield of HBM in the industry. As well as the increase in memory demand driven by AI servers, which drives the proportion of HBM in the overall DRAM production capacity and output value to increase year by year. It is expected that the proportion of total DRAM production capacity will exceed 10% in 2025, and the output value contribution is expected to exceed 30%.

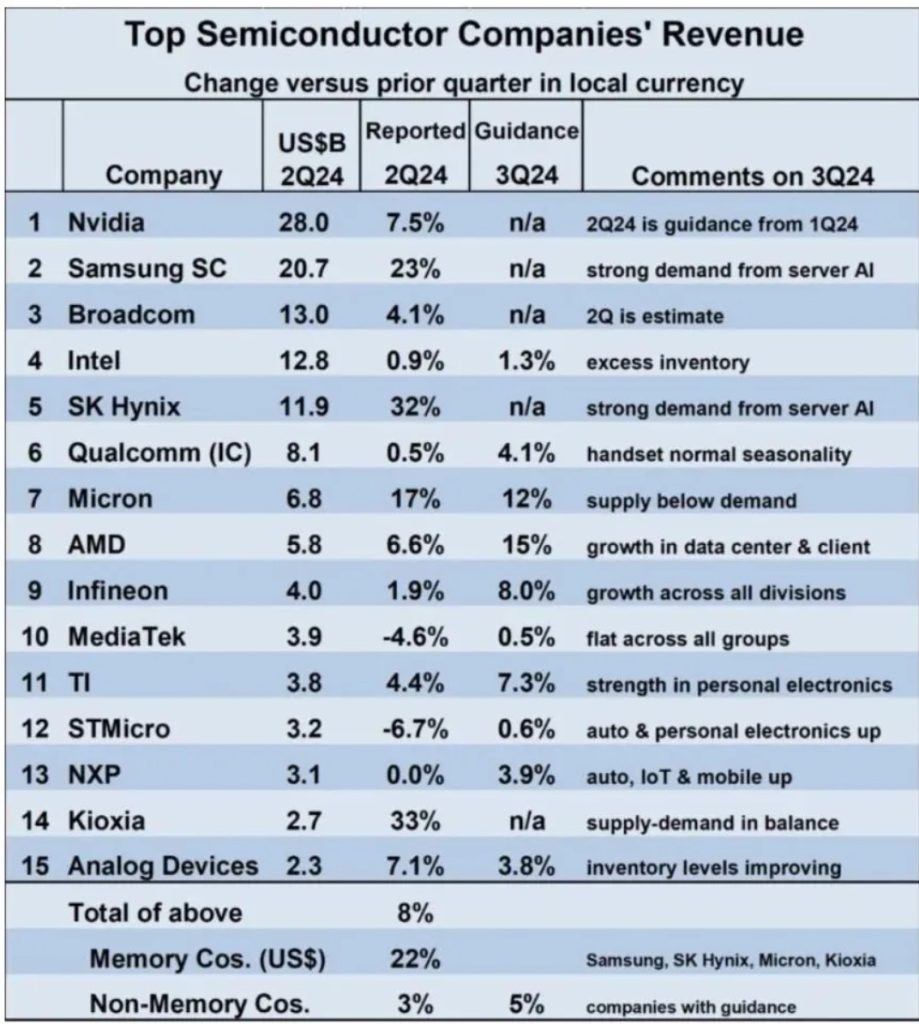

Top 15 IC Enterprises in the Second Quarter: AI Giants Such as NVIDIA and Broadcom Rank at the Top.

According to the news from Kuai Technology, in the second quarter of 2024, the global semiconductor market revenue reached 149.9 billion U.S. dollars, a quarter-on-quarter increase of 6.5% and a year-on-year increase of 18.3%. The WSTS report shows that the revenues of major global semiconductor companies generally increased in the second quarter. Among the top 15 companies, only MediaTek and STMicroelectronics saw a decline in revenue.

Memory companies performed strongly. The revenues of SK Hynix and Kioxia increased by more than 30% respectively. Samsung Semiconductor rose by 23%, and Micron Technology rose by 17%. NVIDIA’s revenue in the second quarter was 28 billion U.S. dollars, continuing to lead the industry. Samsung followed closely with 20.7 billion U.S. dollars. Broadcom expects revenue of 13 billion U.S. dollars, exceeding Intel’s 12.8 billion U.S. dollars, pushing Intel down to fourth place.

The revenue outlook for the third quarter is optimistic. AMD expects a 15% growth. Micron expects a 12% growth in the memory market. Samsung and SK Hynix expect continued growth in server artificial intelligence demand. In the first half of 2024, the semiconductor market increased by 18% year-on-year. The full-year growth expectation is 17.0%.

Post time: Aug-27-2024